AI-assisted issue detection

Built into the CreditSoft product direction so the public site, portal, and office node stay connected.

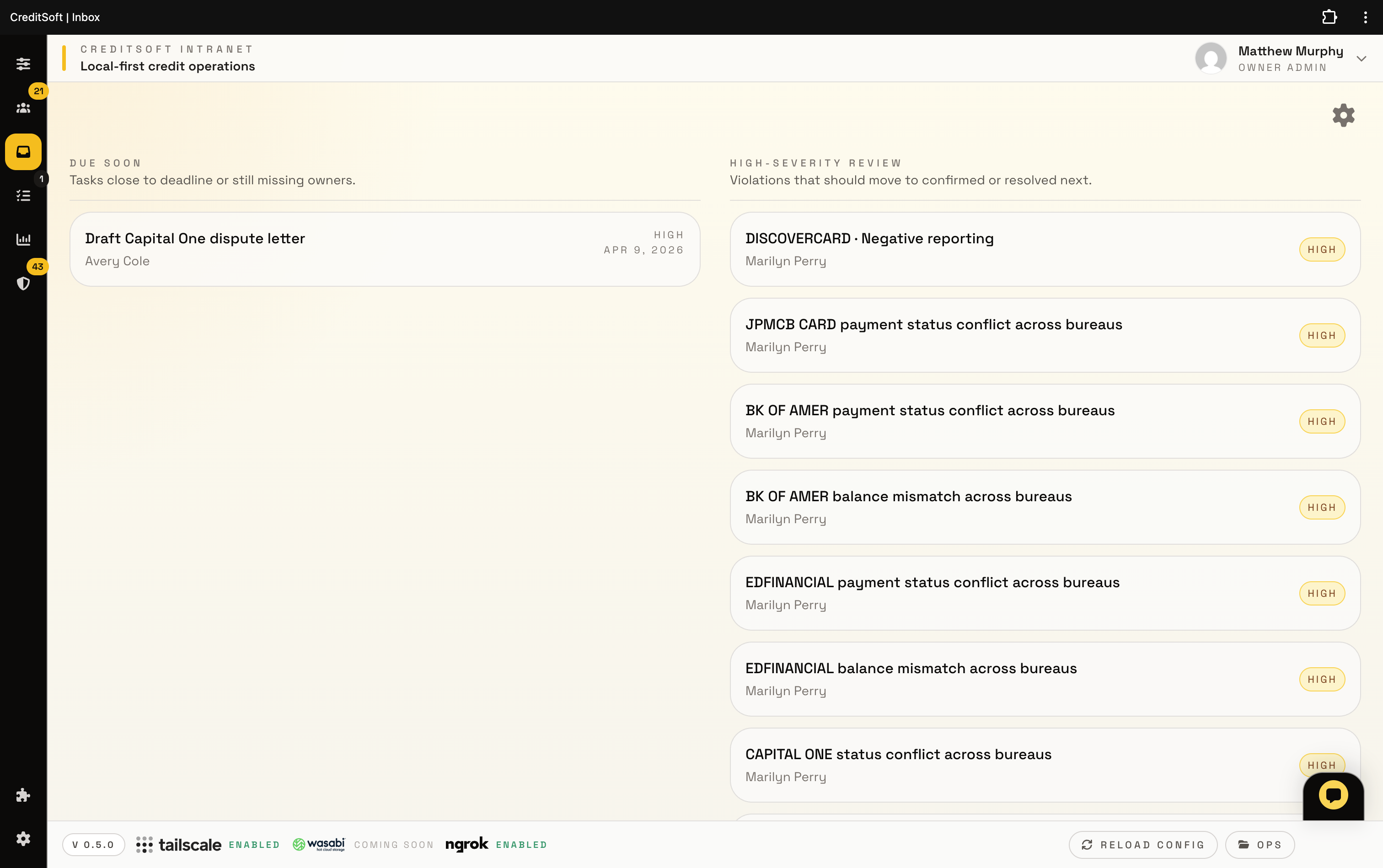

CreditSoft is shaped around Metro2 issues first, then letters and workflows follow the data instead of generic template guessing.

Click the screenshot to open the full-size shadow-box view. This page should never feel like a text-only placeholder when the feature menu sends someone here.

Built into the CreditSoft product direction so the public site, portal, and office node stay connected.

Built into the CreditSoft product direction so the public site, portal, and office node stay connected.

Built into the CreditSoft product direction so the public site, portal, and office node stay connected.